While consumers wade through the ever-ballooning list of brands wanting to wash their clothes, clean their homes, park their cars and deliver them dinner, a newer crop of startups has begun catering to the needs of those contract workers who make the on-demand economy possible.They’re smart to be zeroing in these independent contractors. On-demand employees represent a huge and growing wave of people who now operate as free agents, with the freedom and flexibility — and often instability — that’s part of life without a corporate parent. In fact, Intuit has somewhat famously predicted that fully

40 percent of U.S. workers will be “contingent” workers by 2020.

Patricia Nakache, a general partner at Trinity Ventures who has led deals in on-demand companies, including Eat Club, calls 1099, or contract, workers part of a generational shift. “Millennials are much less receptive to the monolithic education or work-experience notion that, ‘I’m going to have this job with a single company for 10 or 12 years or take all my classes from one-four year institution,’” she says. “They’re really beginning to question the boundaries of those experiences.”

And VCs have begun meeting with companies that cater to them.

For example, Homebrew cofounder Satya Patel points to several companies that hope to serve the most immediate needs of contract workers — which, in most cases, is frequent and steady work. Peers, for one, a San Francisco-based, still-in-beta startup launched by RelayRides founder Shelby Clark, wants to make it easier for people to find, compare and manage on-demand work opportunities. (It also points them to tax, financial and legal resources.) Kung Fu, an eight-month-old San Francisco-based company, is similarly building a platform to help people earn income based on their location and skills.

“I definitely think there is a major opportunity” here, says Patel.

Nakache is meanwhile seeing more startups approach contract workers from specific service angles. One such group are applicant tracking systems startups that — unlike predecessors catering to larger companies — are designed for batch processing. OnBoardIQ, an eight-month-old, San Francisco-based outfit, is among the newest startups trying to streamline the process hiring hundreds of people quickly. Playbook HR, a 10-month-old, San Francisco-based company, also began life as an applicant tracking system (though, sorry investors, Intuit acquired it in March).

According to Nakache, WorkPop, a year-old, L.A.-based company that’s been building a marketplace for hourly workers to find food and retail jobs (and which Trinity has backed), is beginning to eye the category, too.

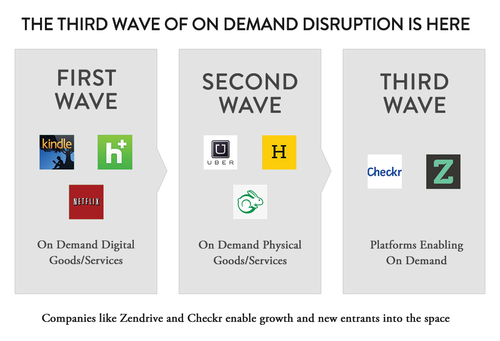

A separate group of companies has sprung up around background checks. One of them is year-old, San Francisco-based CheckR; another is three-year-old, London-based Onfido. While background checks are nothing new, the industry hasn’t traditionally needed to act quickly or process large numbers of people at once; meanwhile, newer companies are only too happy to do both, even if their predecessors aren’t readily ceding the territory. (Uber, the ride-hailing company, uses Hirease, a 13-year-old, Southern Pines, N.C.-based company, to vet its drivers. Competitor Lyft similarly uses a more established company, 40-year-old, New York-based SterlingBackcheck.)

Yet there are other types of companies catering to the specific needs of contract workers.

Don’t be surprised to see more shift-planning startups like five-year-old, San Francisco-based ShiftPlanning and four-year-old When I Work in St. Paul, Mn.

Payroll startups that make it easier for contractors to get paid are also springing up, from four-year-old ZenPayroll in San Francisco, to 1.5-year-old Tiempo in Sunnyvale, Ca.

Of course, healthcare — which most contract workers don’t receive from their employers — may represent the biggest opportunity of all. Among the startups beginning to eye the space: two-year-old, San Francisco-based Stride Health, a health insurance recommendation engine that’s targeting the needs of small businesses and sees 1099 workers as a potential source of business.

There are so many startups beginning to target 1099 workers, in fact, that Nakache says Trinity has yet to pull the trigger on a related investment. She doesn’t expect it will be long, though.

“We haven’t found quite the right fit for the stage at which we invest,” she says. “But it’s safe to say that we’re actively looking and actively engaged in the sector. We have a lot of companies on our radar screen.”

Almost a year-and-a-half after Ali Rowghani resigned as COO of Twitter, he’s been appointed the head of Y Combinator’s growth fund by the organization’s president, Sam Altman.

Almost a year-and-a-half after Ali Rowghani resigned as COO of Twitter, he’s been appointed the head of Y Combinator’s growth fund by the organization’s president, Sam Altman.