By Craig Hanson

By Craig Hanson

The most disruptive aspect of capital market shifts isn’t simply that financing your business becomes easier or harder. It’s that the underlying math the market uses to value your company fundamentally changes. Public markets, venture capitalists and even employees evaluate you through a different framework. These shifts can be dramatic, with severe consequences for those still adhering to the prior paradigm. The market is reminding us of the potential for one of these systemic shifts now.

For the past couple years, investors of all stages have been chasing furiously after high-growth companies, and rewarding them with valuation multiples exponentially higher than the difference in their growth rate would otherwise imply. An almost single-minded obsession on growth rates has understandably driven companies to dramatically increase their sales and marketing spending, faster than historical norms, fueled by round sizes larger than historical norms.

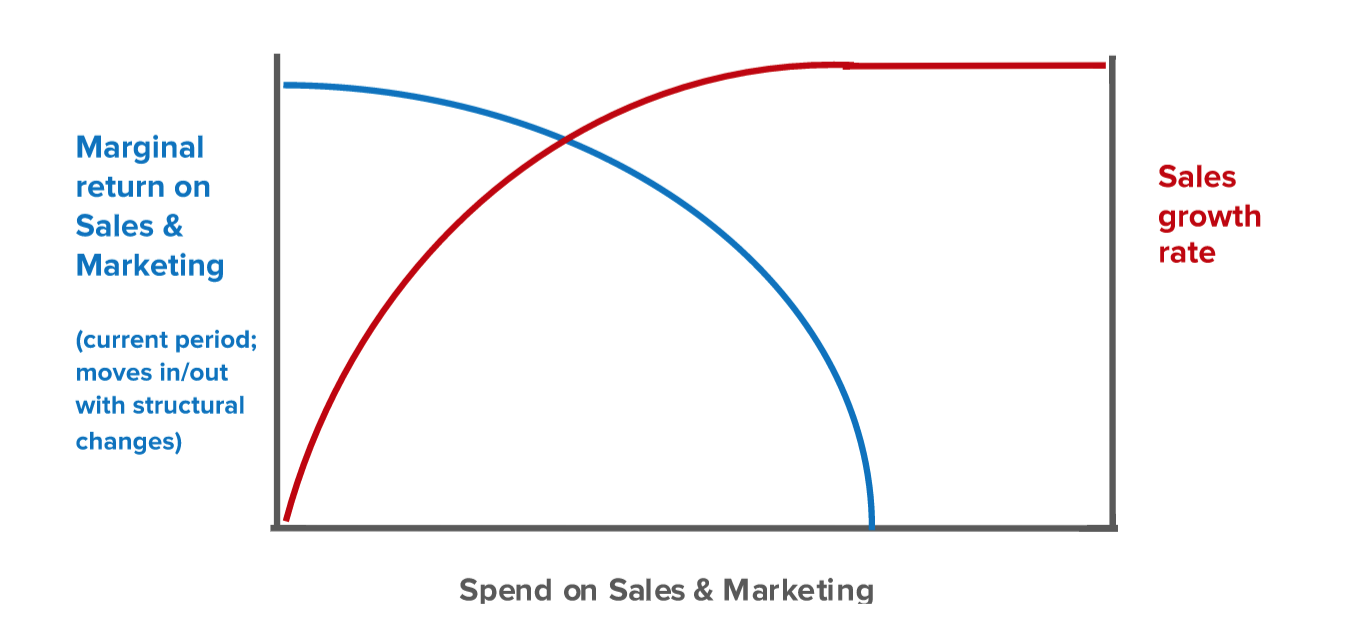

The constraint, however – the gravitational impact of expansion economics – is that as more sales and marketing budget is spent in a period of time, the efficiency of that spend (in terms of qualified leads, sales prospects, sales, etc) naturally declines. This law of diminishing marginal productivity makes sense when you stop to think about it. When you move from the top 10 ROI marketing programs to the next 20 down the list, you’re investing in lower return programs. If you see 50 sales rep candidates in a quarter, and move from hiring the top 5 to hiring the top 20, you’re going to get lower productivity reps (assuming the manager is good at picking reps in the first place).

Despite this, in the recent environment, CEO’s have felt immense pressure, and a bit of economic rationale, in increasing sales and marketing spending even as the productivity of those dollars declines. In other words, even as it drives productivity and efficiency metrics down, some CEOs keep stepping on the gas. Why? There are 2 reasons: one bad and one (temporarily) good.

First the bad reason. Foremost, as some investors are pumping up round sizes, at all stages, much higher than normal, CEOs given this largesse naturally feel immense pressure to spend it. In too many cases, they have to increase spending dramatically in order to have any hope of reaching the herculean growth rates needed to justify the lofty valuation they just received. Shooting the moon is the only play in the book which has hope.

There is a second reason, which has slightly more economic rationale, but only temporarily. CEOs may calculate the exponential increase in valuation multiple they receive for an extra 10% of annual growth, relative to the diminishing marginal impact of the sales and marketing money they’re spending. In essence, even though that next dollar spent on sales and marketing is getting you less and less revenue impact, that little bit of revenue impact is still getting you up the exponentially-increasing valuation multiple curve, enough to still justify it.

The problem with this calculus is this: The diminishing marginal productivity curve is fairly constant, and only increases or decreases over time with the structural effectiveness and size of your programs. This takes time and concerted effort to change. The valuation reward curve, however, is entirely market dependent, and can fluctuate on a dime. In other words, the extra premium you think the market will give you for all of that extra sales and marketing spend can go away. With the recent market drops, this is a shocking wake up call for some CEOs who thought the valuation-for-growth math was a constant.

Historically, this is exactly what happens to companies when market preferences shift. Those of us who’ve been through a couple cycles remember this full well, but many CEOs and even VCs today weren’t around the last time the math changed unexpectedly.

In most market stages, public and private market investors care about both growth and the cost of that growth. The metrics of your company’s growth tell the story of its effectiveness, and thus of its sustainability. It’s not just about the growth – it’s how you get there that matters in the long run.

By taking on mega-rounds, CEO’s should know that they’re doing three things: (1) narrowing their range of operational plan options, as going for broke is the only thing that can work; (2) putting increased pressure on their company to perform to match those expectations, because anything less will eventually create a negative spiral of down-rounds, underwater employee options, and employee defections; and (3) having to hit these high performance standards while slipping lower and lower down the marginal productivity curve.

Worse yet, we see a lot of companies approach us looking for a round much larger than normal as a means to jack up the growth rate and improve the metrics. These are the companies I run from. It shows CEOs who don’t yet have the model working well, have usually achieved good but not exceptional growth, and yet want to spend their way even further down the marginal productivity curve.

In my view, there can be a place for large financing rounds. But that time is once you have the metrics humming, a well-returning place on the productivity curve, and the discipline to spend at a pace the company can soundly keep up with.

How are we handling this at our venture capital firm? Admittedly, as expansion stage investors (typically Series B,C,D), we get to rigorously analyze early performance of the company’s model. We pay attention to the productivity and efficiency, and then work our fingers to the bone helping CEOs improve this further as they ramp up the growth curve and move the marginal productivity curve forward over time. We respectfully pass on companies where the model isn’t working or where the CEO doesn’t know what has to be done to build a well-oiled model. Those CEOs who know how to read the metrics of their business and have an astute sense of how to turn it into a powerful platform as they ascend up the expansion stage have our respect and loyalty.

In most market environments, and perhaps now once again, markets care about both your growth and how you get there. CEOs who pay attention to the fundamental strength of their operating model will guide their companies well no matter what the macro markets do. They know that metrics matter.

As markets have reminded companies before and now once again, those who sacrifice metrics for growth shall eventually have neither.

Craig Hanson is the cofounder of Next World Capital, a San Francisco-based expansion-stage venture firm.